How do you start buying your first Omaha NE home? The hardest part about buying…

What is Debt-to-Income Ratio? | Omaha NE Home Buyer’s Guide

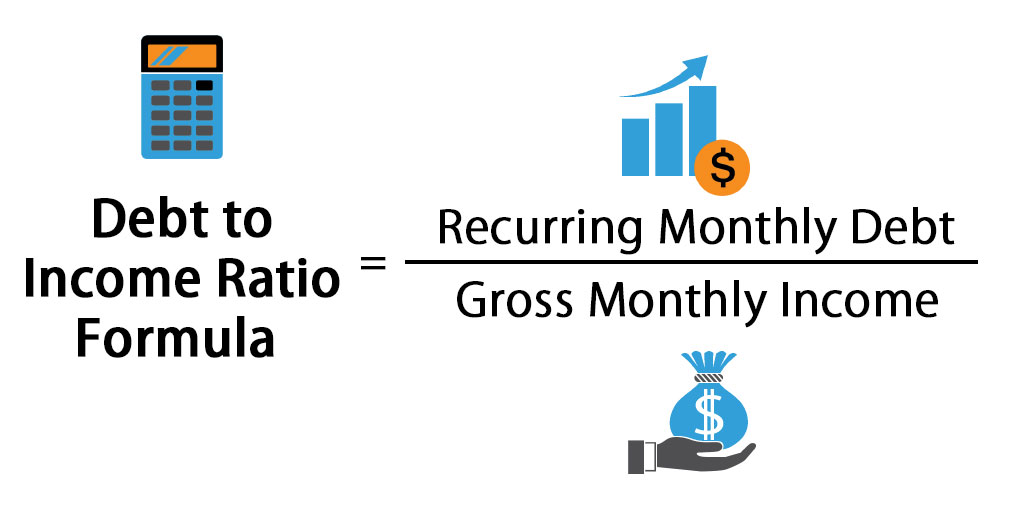

If you are buying a home in Omaha NE, here is what you need to know about DTI.

Debt to Income ratio is used to determine how much house you can afford. To determine your DTI, we will take the new mortgage payment, including taxes and insurance, and all debts that appear on your credit report. These payments will be compared to your monthly income to determine your max purchasing power.

We are a local mortgage broker serving Omaha, Papillion, La Vista, Bellevue, and all of eastern Nebraska. If you have further questions on debt to income ratio or would like to know how much house you can afford please contact us.

Find out your Purchasing Power HERE

- How do you calculate debt to income ratio?

- What is a good percentage of debt to income ratio?

- How can I lower my debt to income ratio quickly?

- Is rent included in debt to income ratio?

How do you calculate debt to income ratio?

For income

For any home loan your income is calculated using your gross income. We will first determine your monthly income before taxes, health insurance, or retirement funds. We take your base pay before any thing is deducted for your monthly income. Receiving bonus, overtime, or commission (or are self-employed) requires we dig a bit deeper to get the final calculation on gross income.

For debt

For your debt ratio we will take the new house payment (principle, interest, taxes, insurance, mortgage insurance, and homeowner’s association dues) for your housing debt ratio. We will then look at the minimum payments on all debts showing on your credit report. We will also take monthly obligations on child support, alimony, tax or judgement lien payments. These monthly minimum payments will be your total debt ratio.

To calculate your debt to income ratio we need to see what your percentage of your income is going to pay all these monthly debts.

A few ways to adjust your debts

There are a few things to consider when calculating monthly debt obligations. There are actually a few debts that have payments that we may not need to count and there are a few debts without payments that we will have to factor into your debt ratios.

Debts we can remove

With an installment loan (car loan, unsecured loan, or any fixed term loan) debt is removed if it has less than 10 payments left AND the monthly payment is not more than 5% of your monthly gross income. There are a few variations of this rule for different loan programs so it is important to consult with a mortgage loan officer before removing this from your debt calculations.

Debts that must be added

One of the biggest issues with debt ratios for new home buyers is their student loan obligations. Many new home buyers have a sizable amount of student loan debt that they may not be making payments on at the time the buy a house. However, this does not mean we do not have to include them in your debt ratios. If you have a current loan in deferment we will still have to estimate the future payment on that student loan and use it to calculate your purchasing power. Depending on the loan program, this can be between .5% and 1% of the total balance. If you have a $100,000 student loan, even if it has no payment, we will likely have to use between $500 and $1000 a month in payment. For many buyers this will drastically reduce their purchasing power or disqualify them from financing all together.

There are some exceptions to this rule so if you do have student loan debt contact a mortgage loan officer to discuss options.

What is a good percentage of debt to income ratio?

Every loan program has different max debt ratios they will allow and most are a bit flexible if the borrower has compensating factors. But typically you want to keep the new house payment at 35% of your gross income and the total of all debt payments at 45% of your gross income.

Every loan program is different

Traditional financing, called conventional loans, is going to be the most strict on debt ratios. The conventional program will generally keep you at the 35/45 unless you have compensating factors. Under no circumstances will they go higher than 50% of the total debt ratio.

FHA and VA, called government loans, are a bit more flexible. FHA will go as high as 56.99% on the total debt ratio and VA relies heavily on compensating factors. VA will go extremely high on debt ratios if the buyer has other factors that make them a good lending risk.

Compensating factors

A compensating factor is something outside the debt and income that will make you a good credit risk. A buyer is more likely to qualify with higher debt ratios if they have reserve assets (assets available but not used for the loan), a higher down payment, or excellent credit. With one or more of these compensating factors, you can get approved with higher than average debt to income ratios.

How can I lower my debt to income ratio quickly?

I always stress the importance of speaking with a mortgage loan officer as early in your home buying journey as possible. A big reason for this is the debt to income ratios. With a bit of time we can work on quickly getting your debt to income ratios in line for a home purchase.

Paying down credit card debt

If your total debt ratio is a bit high, we can do a review of your credit and figure out the most efficient way to get your monthly payment obligations down. This is not just a matter of paying down credit card debt, but figuring out which ones are the best to pay down to get the most “bang for your buck”.

For example, if you have a Von Maur card with a balance of $1000 but a monthly payment of $100 that is the better option than a credit card with a $5,000 balance and a $75 a month payment. We will look for cards with a low balance but high relative minimum monthly payment. Using this method we will be able to get your debt ratios down for a minimal amount of money.

Refinancing a car

If you have an active car loan we could explore refinancing it to a lower rate or longer term. A car refinance is a quick and cheap process that can lower your monthly obligations several hundred dollars. If you have improved your credit since taking out the car loan the difference can be drastic. For example, a buyer that worked very hard to get his scores up to 700. His active car loan was taken out when his scores were in the 500s and the rate was over 19%. We were able to refinance it to less than 5% and get the payment dropped by over $300 a month.

If you think you could benefit from a car refinance, I have several contacts here in Omaha that can help get you qualified for new financing.

Paying an installment loan down to less than 10 payments

As mentioned before, in some cases an installment loan with less than 10 payments can be removed from the debt ratios. With just a little more than 10 payments left, we could wait until it gets to less than 10 or you could make extra payments to get it down to less than 10 payments.

Income based student loan payments

A few select loan programs allow us to use “income based” student loan payments rather than .5% to 1%. In these cases you would just have to apply for income based repayment and wait for it to be approved. This can make a massive difference in your monthly obligations and can improve your purchasing power.

This option can take a few months to get in place so if you think this is a possibility for you please reach out as soon as possible to qualify.

Want to know more about lowering your debt ratios go HERE

Is rent included in debt to income ratio?

If you are currently rent and want to know if you current rent is included in your debt ratios I have good news….It is not. Any housing obligations you currently have will not be counted. If you plan living in the new house we do not have to count current rent.

Can I rent out a room to lower the debt ratios?

Another common question is can we use “boarder income”. The short answer is “rarely”. Any income used to qualify for a home must come from the people on the loan. Only a few select programs allow rent from a roommate to be used and extensive documentation is required. The renter cannot be new so we must have proof that they have rented a room from you for the last 12 months. This renter must have paid you directly with a check or other forms of documented rent.

Debt to income is one of the more complex parts of a home loan approval and there are many ways to work it. If you are thinking of purchasing a home and are concerned about your debt please contact us.

Other useful links

- How to improve your credit

- The 20% down rule on conventional

- What is Escrow?

- How is income calculated?

- Why your assets matter

- Mortgage Calculator

- Is Credit Karma accurate?

- FHA vs Conventional, which is better?

What To Do Next

Related Posts