Most people think selling their home over the holidays is a bad idea. The house…

What is Loan-to-Home-Value? | Omaha NE Home Buyer’s Guide

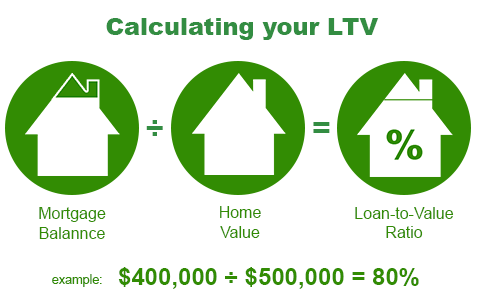

How does Loan-to-Value work on a home purchase?

Loan to home value is the difference between the value or purchase price of your home and the loan amount you are taking out against it. If you have a $200,000 house and a $160,000 loan amount, you have an 80% LTV (Loan-to-Value) on your home.

I am a local mortgage broker serving Omaha, Papillion, Bellevue, La Vista, and all of eastern Nebraska. If you have any questions on buying or refinancing a home, I can help.

Want to know how much house you can afford?

- Is a lower LTV better?

- How does LTV effect the interest rate?

- Does a lower LTV change mortgage insurance?

- What is the highest LTV allowed?

- Should you wait to purchase until you have more down?

Is a lower Loan-to-Value better?

For a purchase

Putting more money down on a purchase will lower the loan to value on your home loan. This does have benefits. But there are a few things to consider before putting all your money towards the down payment.

Do you have other debts with higher interest?

Many buyers come in and want to put as much as possible towards their new home. I get that it can be scary, especially for first-time home buyers, to take on such a large new debt, but we need to look at how to best use the funds you have available. Do you have credit cards, auto loans, or installment loans with higher interest? With mortgage rates so low, it might be better to lower your down payment and put that money towards higher interest debt. A few thousand more down on your house might only lower the payment $25 to $50 a month. But putting a few thousand towards your credit card can save you hundreds a month in minimum payment.

Remember you will need money after closing for the house

Even the most “move-in ready” house will have expenses. Those Target and Lowes run you make start to add up. Plan on having a bit of reserve to get yourself into your new home and get it ready over the next several months. It is also good to plan for minor repairs. While this can vary from house to house, a good rule of thumb is to expect 1% of the purchase price in maintenance each year.

For a refinance

On a refinance a lower loan to value is almost always much better. If you are looking to refinance the first thing we have to do is look at the updated value of your home and compare it to the current balance of your mortgage. If you bought the home several years ago with a small down payment or with a first-time home buyer loan, you might now be in a position to look at other loan programs.

How big is your loan?

The size of your loan matters. All refinances have fees (those ads for no fee loans are just rolling the fees into the rate) so we need to determine if those fixed costs are going to be made up with the savings on a refi. The larger the loan the greater the savings for a lower loan amount.

Find out how much you can save on a refinance

Possible appraisal waiver with higher LTV on a refinance

One other big benefit of having a lot of equity in your home on a refinance is the possibility of an Appraisal Waiver. On a conventional loan (FHA and VA do not give appraisal waivers) the automated underwriting system will review the new loan balance and, if it can determine an automated value, it can waive the appraisal requirement. This will save you some money and time on a refinance. The more equity you have the more likely you are to get that appraisal waiver.

How does LTV affect interest rate?

A lot of people think that the rate is better the more equity they have in the home. While this can be true, it is not nearly as much as most people think. Interest rates are based on risk and there are already things in place to reduce the risk for lower LTVs on most loans.

Conventional financing

A conventional loan will require mortgage insurance on any loan with an LTV higher than 80%. If you are buying or refinancing into a conventional loan, you will be required to have MI if you do not have 20% equity. Now this mortgage insurance is not insurance for the buyer/borrower. It protects the lender from losses. Because of this insurance, the risk for lower LTVs is reduced to the lender so they do not have to increase the rate. However, on conventional mortgage insurance does increase with lower loan-to-values. If you have 15% equity in the home the mortgage insurance is going to be less than if you have 5% in the loan. So the rate does not change, but the MI does on conventional.

FHA and VA financing

Both FHA and VA are considered “government loans”. At least that is what we call them. They are loans guaranteed by either the Federal Housing Administration or Veteran’s Administration. These guarantees reduce the risk to the lender no matter how little equity you have in the home. Typically on these loans the rate does not change based on a lower LTV. Just like conventional, FHA and VA have their own version of mortgage insurance and it is reduced slightly with more equity. However, it is not nearly as much as the conventional reduction. You can expect small savings for a lower LTV with FHA and VA.

Does a lower LTV change mortgage insurance?

I covered this in the previous section, but I want to go into a bit more detail about how mortgage insurance works on a home loan.

Conventional Mortgage Insurance

This is the one that is most effected by a lower LTV. If you are putting down 3% on a conventional home purchase you can expect higher mortgage insurance than if you were putting down 10%. The mortgage insurance is based on a percentage of the loan amount, but that percentage is reduced with a lower LTV. There are several other factors that go into determining the exact mortgage insurance percentage (credit score, number of buyers, etc). But do give you an example, let’s say you were buying a home for 200k and putting down 3%. Your MI might be .7% of the loan amount per year or $1320 on a loan amount of 196k. If you were buying a 200k house and putting down 10%, the mortgage insurance might be .25% of the loan or $450 a year on a 180k loan.

Go here to get a quote on mortgage insurance

FHA and VA Mortgage Insurance

Now FHA and VA do not call their insurance “mortgage insurance”. They have funding fees, but they serve the same purpose. VA has a flat fee that is rolled into the loan at close. This fee is reduced with a 5% down payment and it is reduced more with a 10% down payment. FHA’s “mortgage insurance” changes very little with a larger down payment. Currently, FHA charges .85% of the loan amount per year in MI. If you put down 5% or more that drops to .8%. Not a huge difference.

Many buyers want to avoid MI at all costs. This is understandable. It is a benefit to the lender, not to the buyer. But there are reasons that paying the mortgage insurance and buying now is more beneficial than waiting until you have the larger down payment. The only way to really know your situation is to do a consultation to see where you are at currently with your income, assets, debts, and credit score.

What is the highest LTV allowed?

The highest allowable loan to value is different for each loan program. I go over down payment requirements in many other articles so here I want to go over how a low loan to value is a positive compensating factor on a loan.

Conventional LTV

A compensating factor is something that improves the overall approval of the loan. A strong compensating factor in one area (say a low LTV) will allow you to be less than perfect in other areas of the loan.

Conventional loans must be run through their AUS (Automated Underwriting Systems) this is an automated review of all aspects of the loan application. It reviews credit, income, job history, assets, down payment, and real estate currently owned. This automated evaluation determines if the loan is eligible for conventional financing. The loan officer and underwriter just need to verify that all the information entered was accurate and the buyer gets their financing.

These AUS are always changing exactly how they evaluate a loan application, but it does take into account a buyer that is strong in one area but weak in another. For example, if you have a debt to income ratio you may not qualify for a 3% down conventional loan, but you may qualify for a 10% down loan. That lower LTV was your compensating factor.

FHA and VA LTV

The FHA and VA program have their own AUS and operate somewhat like the conventional automated underwriting. Compensating factors are still a factor for both FHA and VA. However, FHA and VA are both designed to be low down payment programs. So a buyer could have high debt ratios, limited assets, and lower credit scores and still qualify with little or no equity in the home.

For buyers that are buying a home with little down or refinancing with little equity and cannot get an automated approval on a conventional loan, FHA is likely the best option.

Should you wait to purchase until you have more down?

Many people will tell you to wait until you have 20% down on a home before purchasing. If you do have the 20% down, and that is the best use of those funds, that is fantastic. But not having the 20% down should not deter you from purchasing a home.

Buying now with a limited down payment could make more financial sense than waiting until you have the 20% down payment. Even with the monthly mortgage insurance payment, buying now will allow you to build equity rather than renting and waiting. In just a few years you could gain 10s of thousands of dollars in equity that you would not have had if you continued to rent and save up.

Before waiting lets calculate how much a Nebraska home would gain yearly in value and how much you would pay down on a mortgage. We can compare that to your current rent and how long it would take you to save up a larger down payment.

Other useful links

- How to improve your credit

- The 20% down rule on conventional

- What is Escrow?

- How is income calculated?

- Why your assets matter

- Mortgage Calculator

- Is Credit Karma accurate?

- FHA vs Conventional, which is better?

What To Do Next

Related Posts